I created the impossible by launching my algorithmic trading platform. Now, I’m going even further.

How I plan to create a no-code intraday backtesting system

Nobody believed in me when I said I wanted to create a no-code trading platform for retail.

I’ve talked to dozens of professionals. While these senior quants were impressed by the engineering ingenuity, they unanimously agreed that retail investors wouldn’t be interested in an algorithmic trading platform.

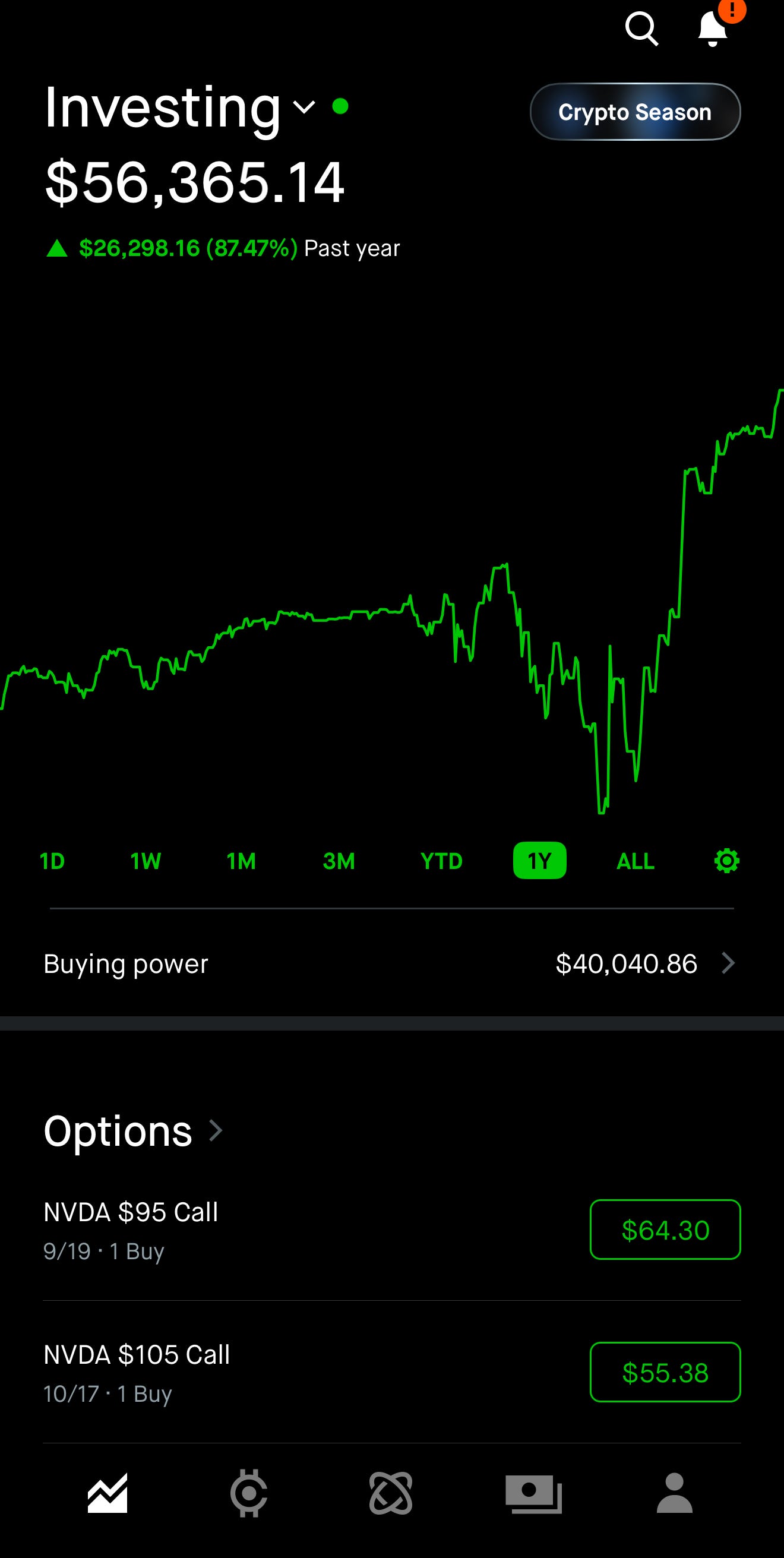

Their lack of faith in me just fueled me. I created NexusTrade, a no-code algorithmic trading platform that can backtest nearly any trading strategy. Strategies can be deeply sophisticated, drawing on technical, fundamental, and economic indicators. I personally use it myself, and I’ve gained nearly 88% in the past year.

I’ve mastered the art of swing trading my particular assets. I focused on NVIDIA and Google, and thoughtfully applied leverage knowing they’re some of the best AI stocks in the world. This strategy worked, and now I’m significantly reducing my exposure by holding a stockpile of cash.

And now as I wait for another buying opportunity, several of the most active users on my Discord have been asking for a particular feature. What if instead of just testing strategies at open and close, we can see how well they perform throughout the trading day?

Here’s a deep dive into my thought process.

What is NexusTrade and its current limitations?

NexusTrade is a no-code platform that allows retail investors to create highly configurable algorithmic trading strategies using natural language.

While NexusTrade stands out among other no-code platforms for being simple and powerful, it shares one common limitation with the other platforms like it.

It can’t test intraday strategies.

When launching a backtest, the platform tests the trading rules out on open and close prices. While great for swing-trading and long-term investing strategies, users aren’t able to test out daytrading strategies at all within the platform.

Equally as important, the concept of an intraday indicator doesn’t exist within the NexusTrade platform.

While strategies like “30 day Simple Moving Average” indicators work just fine, trying to find the rate of change of Apple’s stock in the last 5 minutes is not possible within the platform.

I aim to change that.

The Requirements For an Intraday Backtesting System

My goal is to build a minimal but useful intraday backtesting system. After brainstorming for a while, these are the requirements I came up with:

- Create a system that hydrates intraday stock and cryptocurrency data

- When a user launches an intraday backtest, perform a simulation of the strategy across minutely data

- Allow users to create strategies featuring minutely and hourly indicators

Fortunately, the platform already works well with open/close data. I built an event-driven backtesting system that ingests market data at every timepoint.

I just have to extend it to work with more data. It can’t be that hard, right?

If only it were that easy.

A Data Explosion: The Challenge With Intraday Backtesting

There is a massive problem with intraday backtesting compared to open/closed systems.

The data volume explodes fast.

If we’re backtesting across one year of data, with 252 trading days per year, an open-closed backtesting system will produce around 504 market events.

An intraday system multiplies this number significantly. If we assume regular trading hours between 9:30AM EST and 4:00PM EST, that adds up to 390 minutes in one day.

And for cryptocurrency, that number more than triples, reaching 1440 minutes in a day.

That means, 1 to 2 days of intraday backtesting has higher data requirements than 1 year of traditional backtesting. That’s an insane explosion of data.

A huge challenge with this is that a backtest across a couple of weeks literally won’t fit into the memory of the system. While the traditional system fetches all data before the backtest begins, the new system will need to backtest in chunks, saving results to the database and discarding earlier data as time goes on.

This is MUCH more complicated. Nevertheless, to make a tool that truly stands out, I’m willing to run at full force, tackling this challenge head-on.

Phasing Out This Launch Into Milestones

To launch the MVP of this feature, I’m going to separate it into different milestones.

Milestone 1: Hydrate Intraday Data

- Find a suitable historical data provider for stocks and cryptocurrencies

- Implement a job or process that hydrates the historical data into our database

Milestone 2: Implement the Intraday Indicator

- Support minutely and hourly indicators within the NexusTrade backtesting app

- Allow users to configure the indicator within the no-code UI

- Integrate the new indicator into the AI chat

- Gate the new functionality

Milestone 3: Implement the new Intraday Backtest Function

- Implement needed changes to the backtest emitter including data chunking

- Test that it works for simple buy and sell rules

- Test that it works for complex rebalancing rules

Once these milestones are completed, I’ll launch the feature, starting with premium users and users in the NexusTrade Discord. As I get feedback, I’ll iterate on the feature, evaluate how its performing, and decide if I will launch it to the wider public.

But there’s a chance I won’t. It’s more than possible that the effort for this implementation will go to waste.

The Risks of This Implementation

It’s very possible that after all of this effort, I decommission the feature or leave it only available to select users. Such an ambitious feature isn’t available in other no-code platforms like Composer, and there’s a big reason why.

1. An explosion in cost

Storing this additional data for these backtests may prove to be expensive. Will the usefulness of the feature drive enough subscriptions to handle the increase in data cost?

2. Potential for slow execution

While the algorithmic trading system is implemented in Rust for speed, it’s very possible that intraday backtests of complex strategies to be many orders of magnitude longer than the traditional counterpart. Nobody is going to wait 8 hours for a backtest to finish

3. Disappointing users

Even if these issues, users may just be disappointed that their backtesting results doesn’t translate to real-world trading. Things such as slippage and fees compound when trading more times in a day, and simulating them gets more complex the more trades a user makes. Slippage for a strategy that trades at most twice per day? Not a problem. But every 20 minutes? This is substantial.

Clear disclaimers can be used to level expectations and mitigate the risks. But even with big bold text, users might come out the other end disappointed by the final product.

Oh well. It’s a risk I’m willing to make.

Concluding Thoughts

I built NexusTrade to democratize access to Wall Street-level tools. And now, I’m facing my biggest challenge yet.

Intraday backtesting has the potential to be the most useful, most powerful tool for retail investors to-date. But it comes with substantial challenges and risks. Will the cost be too much? Will users be disappointed with slow speeds and inaccurate results?

I have to find out.

With that being said, perhaps I have tunnel vision, and the risk isn’t worth it. After all, my personal trading account is up nearly 90% without it… is it really needed?

At the same time, imagine the patterns hidden in the sea of intraday data, just waiting to be discovered.

What do you think? Is intraday backtesting worth the risk or should I focus on other impactful features? This can include:

- Options trading, option automations, and AI-Powered options chain analysis

- Futures trading and automation

- Agentic features within the platform

- Enhanced copy trading (for example, copying Nancy Pelosi’s trades as soon as their released)

These are all ideas I’ve heard from users of my platform, but I feel like they can wait. What do you think?

In short, I’ve built a rocket. Now I’m deciding which moon to land on. Should it be intraday backtesting — or something even bolder?

Comment below.

If you have suggestions, requests, or want to be the first to use AI to create an intraday algorithmic trading strategy, join the NexusTrade Discord!

No comments yet.