I asked Claude Opus 4.5 to autonomously develop a trading strategy. It is DESTROYING the market

From Vibe-Coding to Vibe-Trading: Unleashing the Power of AI

When Anthropic released Claude Opus 4.5, I honestly wasn’t excited nor impressed.

Out of the major LLM providers — Google with Gemini, OpenAI with the GPT-series, and Anthropic with Claude, only Anthropic has been aggressively enshittifying their models… aggressively reducing their usage limits to the point where you can’t even use their models within their own platform. In pure frustration, I outright unsubscribed from their service last month.

However, today’s release changed everything. Anthropic smoked their competition with the release of Claude Opus 4.5, and they restored the usage limits that made this model great. While everybody is talking about how great of a coding model it is, one question popped into my mind.

Can it trade stocks?

The final answer blew me away.

How I created an algorithmic trading strategy with an AI Agent?

First, let’s talk about how I created an algorithmic trading strategy using Opus 4.5.

I built a fully autonomous AI agent that can test any trading strategy minute-by-minute by simply describing the rules in plain English.

The way it works is a multi-step process involving planning, research, iteration, and refinement. You can read the technical details behind how she works here.

To summarize the article, the Aurora Agent is powered by the ReAct (reasoning & action) framework for teaching LLMs how to interact with their environment. The agent creates a plan and then executes on it, taking actions, and making observations about the results.

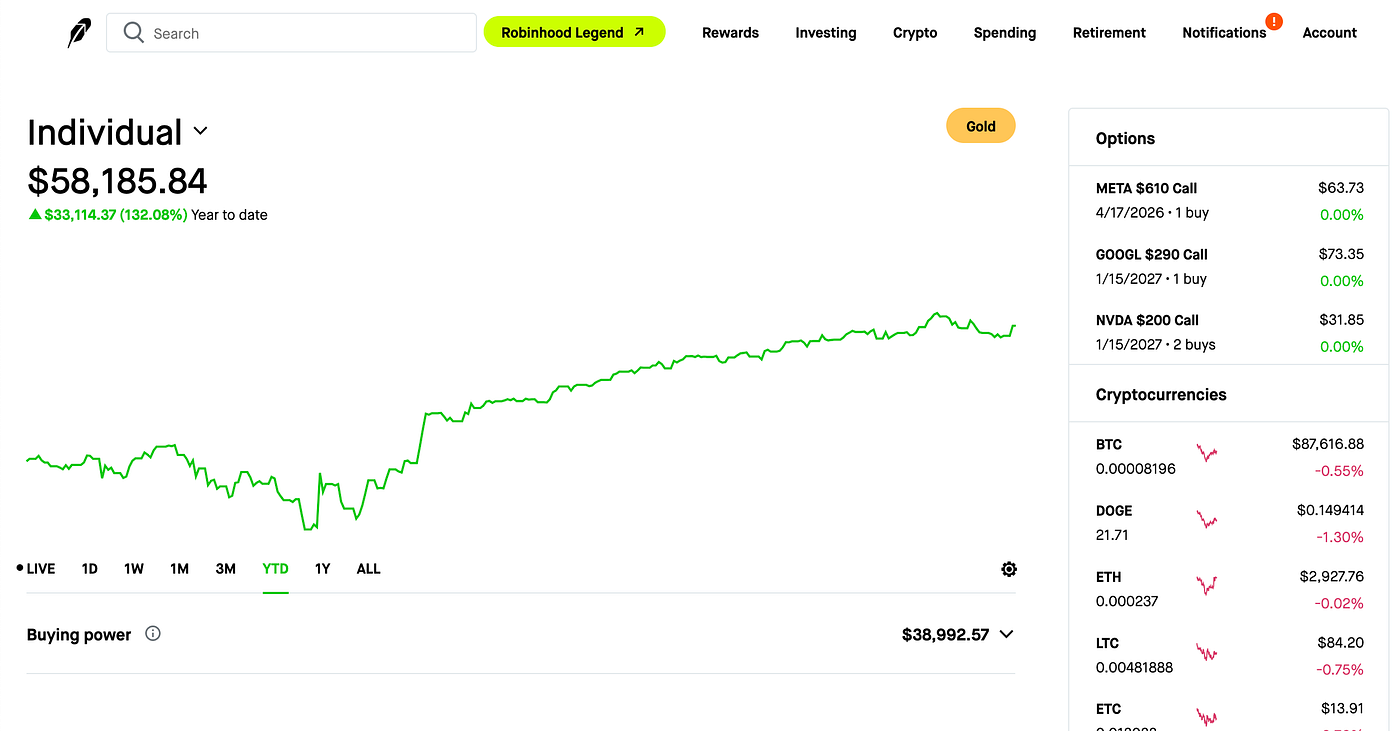

Using the various AI features within NexusTrade, I’ve earned over $33,000 year-to-date, an increase of more than 130% of my portfolio’s performance.

Inspired by my real swing-trading strategy, I asked Aurora to build me the following trading strategy.

I want a profitable trading strategy on TQQQ. I want a take profit strategy, but no stop losses — I’m bullish on tech long-term and don’t want to be stop lossed out. I also want to space out my buys and not go all-in at once. If we can preserve our capital when we (or the broader market) is doing extraordinarily well, and be more aggressive when the market has a major pullback, then I think we can create a great strategy

Aurora didn’t just build one lousy trading strategy. It built a collection of unique ones, each with their own strengths and weaknesses.

But based on risk, raw return, and risk-adjusted return, one trading strategy stood out amongst the rest.

Walking through the Aurora Trading Agent Step-By-Step

The AI goes through a process of planning, testing, optimization, and a final analysis.

Let’s walk through the process together, shall we?

Creating a comprehensive research plan

After sending the initial request, the first thing Aurora did was create a comprehensive plan with four competing hypotheses.

- Hypothesis A (Fixed Profit-Taking + DCA): A simple approach of taking profits at fixed percentage gains (e.g., sell 20% of position when up 50%) combined with regular dollar-cost averaging will outperform buy-and-hold.

- Hypothesis B (Volatility-Adjusted Accumulation): The best approach is to buy more aggressively when TQQQ’s price is significantly below its moving average (indicating a pullback) and take profits when it’s significantly above.

- Hypothesis C (Drawdown-Based Accumulation): Superior returns come from measuring TQQQ’s drawdown from its peak and buying more aggressively as the drawdown deepens (e.g., buy small amounts normally, but buy larger amounts when TQQQ is 20%+ off its highs).

- Hypothesis D (Market Regime + Order Spacing): Combine market regime detection (using SPY or QQQ as a proxy) with strict order spacing rules to prevent over-trading and ensure capital is deployed gradually.

This step is arguably the most important. For different types of ideas, the plan might include screening for fundamentals or performing deep research. The plan guides the agent for the rest of the process.

In this case, Aurora proposed several trading strategies, and an explanation for how it intends to test it.

Then, the autonomous trading agent gets to work.

Testing out different trading strategies

Aurora created a plethora of different trading strategies. In it, it includes holding QQQ and TQQQ to make sure it can outperform the underlying assets.

Then she does an iterative process of creating and testing strategies. It tested the ideas during strong bull markets and devastating bear ones.

While many strategies were promising, one strategy stood out amongst the others. The AI called it Drawdown-Based Accumulation.

The AI then went one step further. It decided to optimize it.

Optimizing the promising strategy

After finding a promising strategy, it wasn’t enough to say “that’s the best we can do”. Aurora decided to optimize it with a genetic algorithm.

A genetic algorithm is a biologically-inspired optimization algorithm that’s capable of improving any performance metric. You can read the technical details behind how it works here.

In this case, Aurora wanted to improve the strategy in terms of raw gains and sortino ratio.

Then Aurora analyzed the optimization results, and tried to see which performed well during training, and whether the performance collapsed out of sample. It found a few promising suspects.

Finally, the AI summarizes the entire conversation, and presents a list of the most promising portfolios for further research and iteration.

Among this is the original (unoptimized) Drawdown-Based Accumulation, a powerful strategy that buys more aggressively during sustained drawdowns.

But let’s put this portfolio to a final test.

How good is the ‘best’ portfolio?

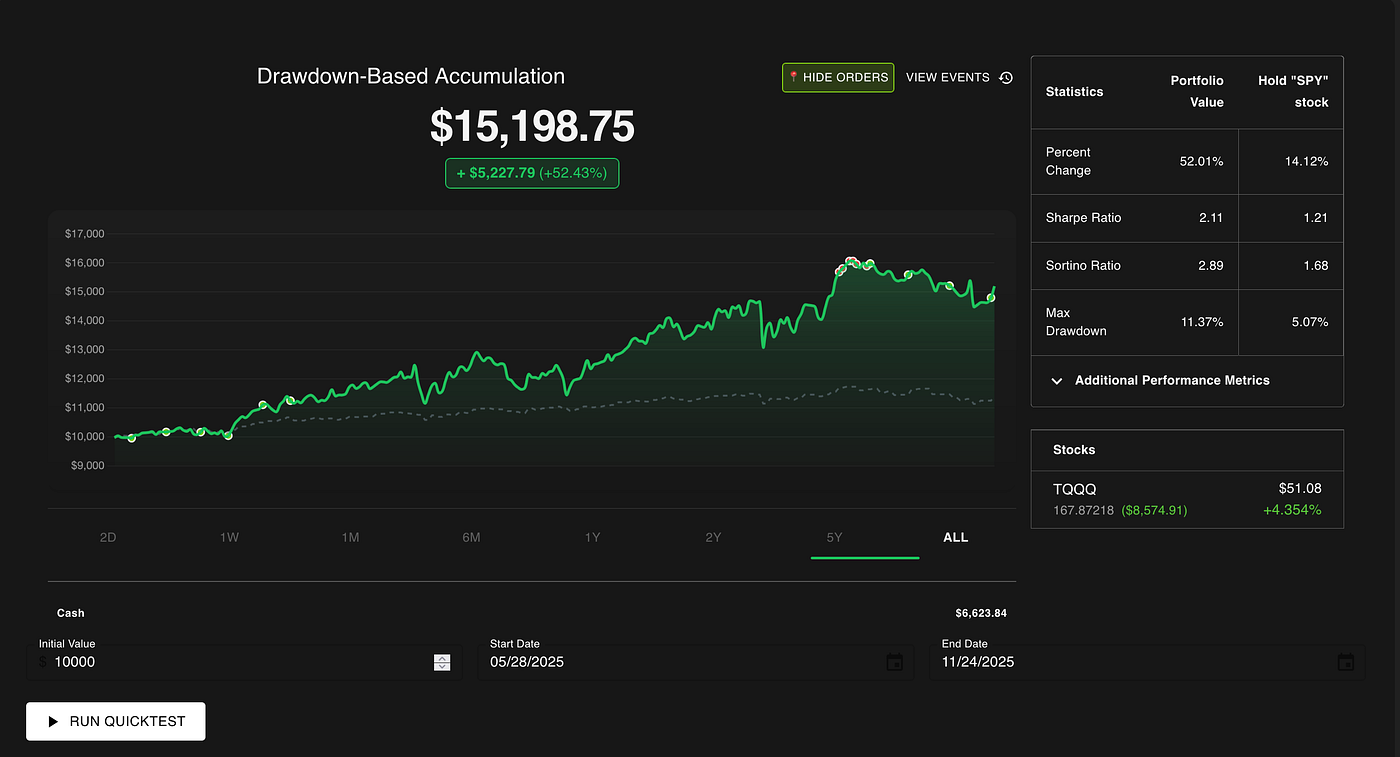

From the entire conversation, Aurora concluded that the un-optimized Drawdown-Based Accumulation Strategy is the most promising. The rules are as follows:

- Buy 300 dollars in TQQQ Stock when # of Days Since the Last Filled Buy Order ≥ 7 and 252 Day TQQQ Max Drawdown < 25

- Buy 1500 dollars in TQQQ Stock when 252 Day TQQQ Max Drawdown ≥ 25 and # of Days Since the Last Filled Buy Order ≥ 5

- Sell 25 percent of current positions in TQQQ Stock when Positions Percent Change > 50

From the initial ‘Quick Test’, this portfolio seems really damn good. From May 28th, 2025 to November 24th, 2025, it earned an outstanding 52%. In comparison, SPY earned a respectable 14%. Good, but not NEARLY as good.

Let’s put it through a REAL test.

- We’ll change the underlying asset to TQQQ to keep it fair

- We’ll test across multiple time periods and see how it fairs

- We’ll give a final, un-biased analysis

Testing from 2020 to 2022

This period was extraordinarily bullish. The results were as follows:

- The portfolio gained 356.3% vs TQQQ’s 275.0%

- It had a sharpe ratio of 1.51 vs TQQQ’s 1.25

- It also had a sortino ratio of 2.07 vs TQQQ’s 1.66

- The max drawdown was 60.8% vs 70.0%

Testing from 2021 to 2023

In contrast, this period was devastating for leveraged strategies.

- The portfolio lost 53.1% vs TQQQ’s -61.8%

- It had a sharpe ratio of –0.15 vs TQQQ’s -0.23

- It also had a sortino ratio of –0.22 vs TQQQ’s -0.32

- The max drawdown was 76.4% vs 81.7%

Testing from 2022 to 2024

This period demonstrates a clear-cut example of a strong pullback followed by a recovery. The performance is as follows:

- The portfolio gained 0.18% vs TQQQ’s -35.3%

- It had a sharpe ratio of 0.37 vs TQQQ’s 0.12

- It also had a sortino ratio of 0.54 vs TQQQ’s 0.17

- The max drawdown was 73.5% vs 80.9%

In this period, the strategy is not barely outperforming the underlying. It’s dominating. Unlike buy and hold, it recovered swiftly compared to just holding TQQQ, breaking even during this recovery.

Let’s do one final test, and see how the portfolio performs recently.

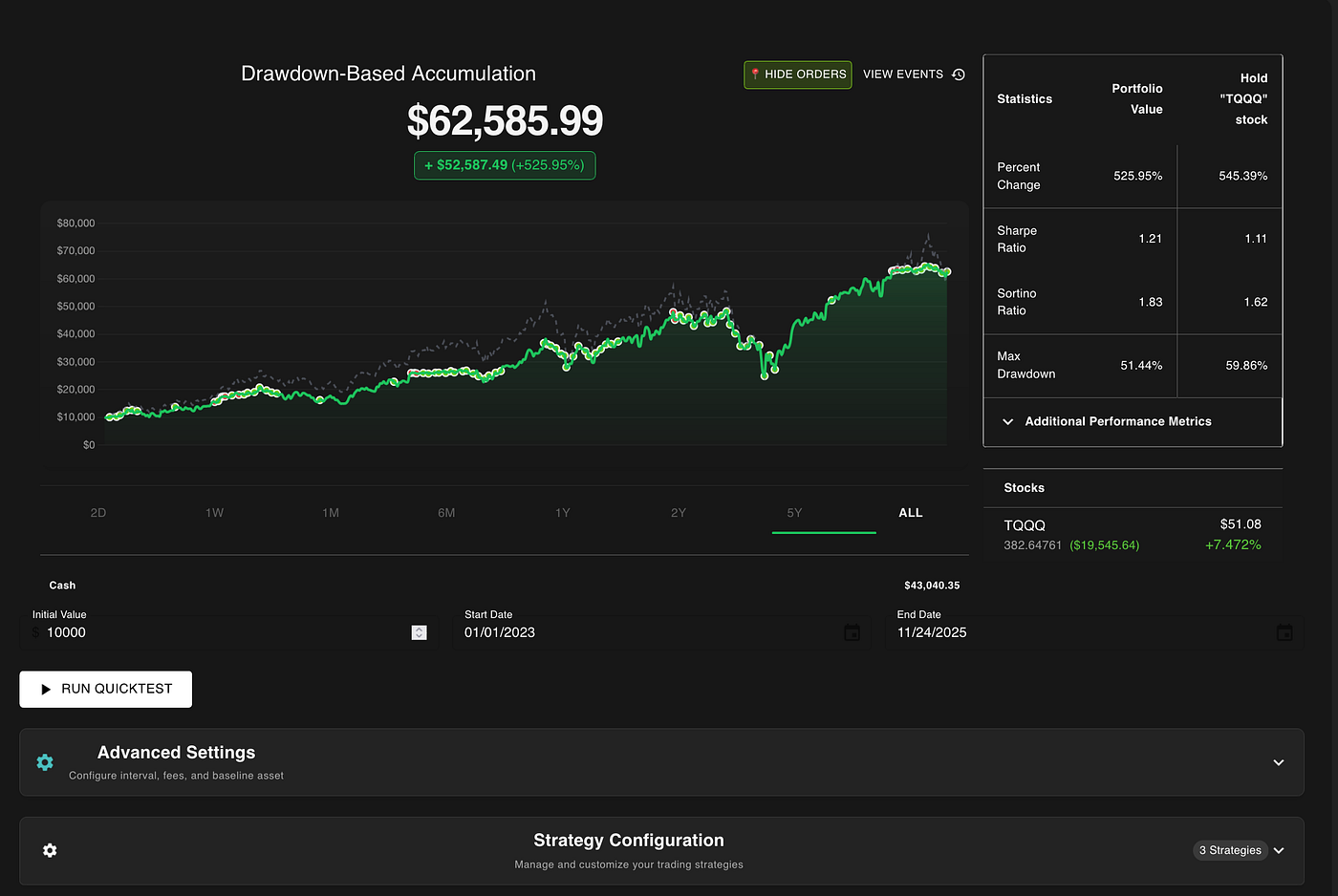

Testing from 2023 to Nov 25, 2025

- The portfolio gained 526% vs TQQQ’s 545%

- But it had a higher risk-adjusted returns, with sharpe ratio of 1.21 (vs 1.11) and sortino ratio of 1.83 (vs 1.62)

- It also had a lower maximum drawdown at 51.4% vs TQQQ’s 60.0%

Final Analysis

The numbers don’t lie and the results are unambiguous. Across these different time periods, the strategy generated by Claude Opus 4.5 was less risky, had better returns, lost less during a bear market, and recovered faster during a bull one.

With a single prompt, Claude Opus 4.5 created a profitable trading strategy. It didn’t spit out words randomly. It mimicked the process of a quant analyst, testing different strategies, optimizing promising ones, and considered trade-offs.

I do want to mention something incredibly important — this isn’t a cookie-cutter strategy that is suitable for everyone. The backtests show this clearly — it lost more than 50% during a bear market and took a full year to recover. A more devastating or prolonged bear market can wipe out an entire portfolio.

This article is simply a demonstration… what happens when you ask an AI agent to create a specific strategy? With this framing, the agent did phenomenal — far better than we could’ve hoped.

The responsibilities of a quantitative analyst have just been automated away, and Claude Opus 4.5 proves it. It’s not a black box where I’m saying “trust me bro”. You can see the power for yourself for free.

The agent can perform financial research, look at correlations between assets, and use technical, fundamental, and economic data to build automated trading strategies.

It’s no wonder that every major financial firm is integrating with AI. Hedge funds are hiring LLM specialists, and professionals are leveraging them to automate financial research.

The proof is clear. If you’re not using AI to help you trade right now, you’re being left behind.

Want to bookmark the portfolio and see its live-trading returns since its deployment on November 25th, 2025? Check it out here.

No comments yet.