Google I/O 2025 Blew My Mind: Why I’m Now Buying GOOGL Stock After My NVIDIA Windfall

I’m still reeling.

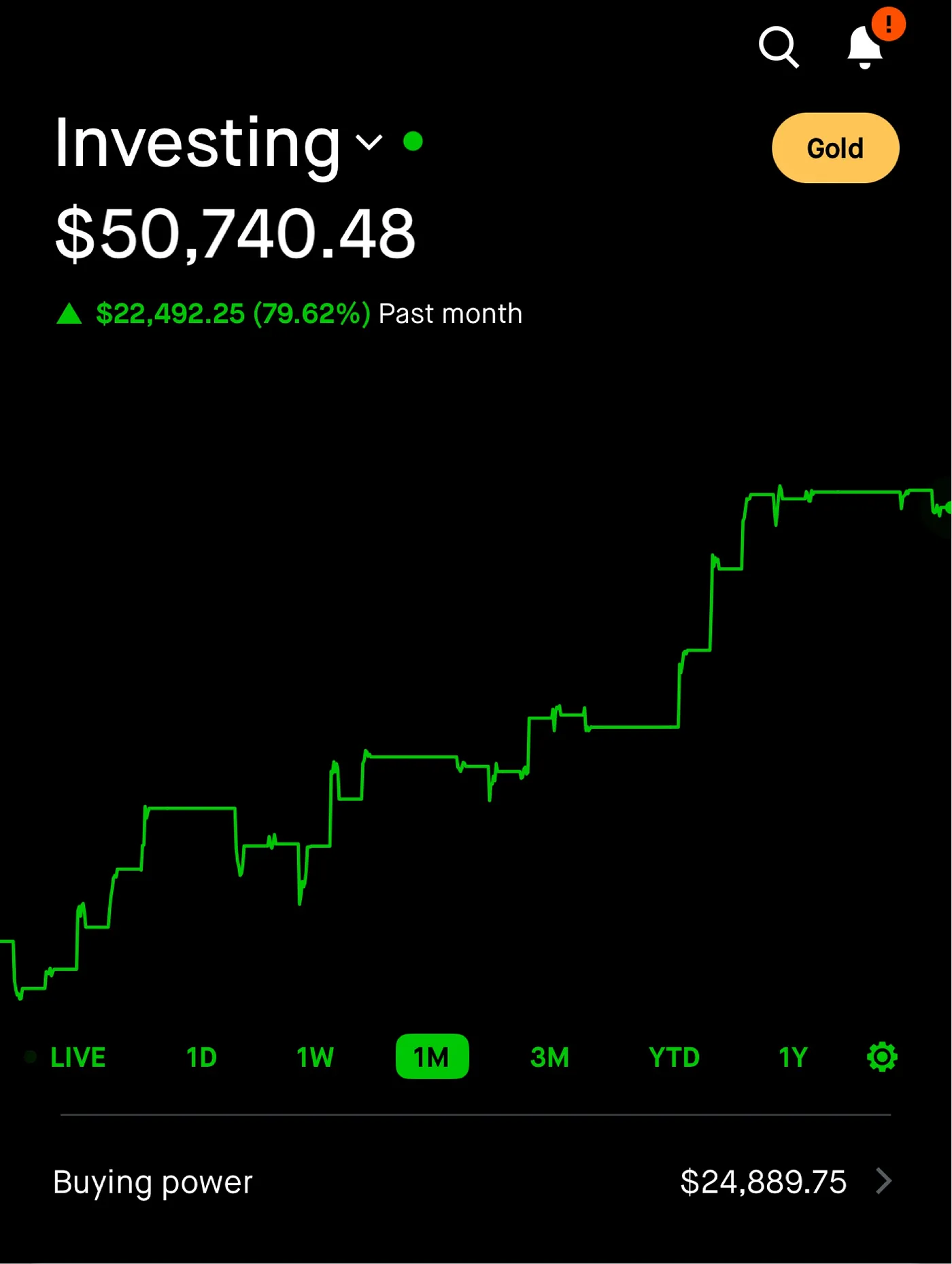

For months now, I’ve shared my options-trading journey with NVIDIA, even when I was hemorrhaging money.

However, throughout the past month, due to some smart (albeit very high risk trades), my account reached its all-time highs, a surge that’s frankly been mind-blowing.

After such a significant win, members of the NexusTrade Discord — a free, Discord for data-driven investors – asked me “What stocks am I planning to buy next?”

Before today, my answer involved taking profits, holding a sizable cash reservoir ($25,000+), and being extremely selective until the Orange Man decides to tank the market again for his billionaire buddies.

But then Google I/O 2025 happened, and I was so astounded by what I saw that I’m starting to dip my toes into a new position: Alphabet (GOOG).

I already knew Google would be a dominant force in the industry. Their models can literally create trading strategies that beat the market and is the #1 most powerful model for SQL Query Generation.

Google’s latest showcase just hammered this point home. I’ve re-entered my position in Google stock. Here’s why.

TL;DR (Too Lazy; Didn’t Read):

- Google I/O 2025 showcased impressive AI advancements including Imagen 4 and Veo 3 that outperform competitors in image and video generation

- Google demonstrates a strong financial position with Q1 2025 revenue of $90.2B and net income of $34.5B

- It is reasonably valued with a P/E ratio of 19.03 (lower than other FAANG stocks, including Apple)

- Innovative “Other Bets” like Waymo self-driving taxis are already operational and expanding

- Thus, I’m investing some of my NVIDIA profits into GOOGL despite regulatory risks and search advertising dependencies

Using AI tools to quickly recap all event highlights

To summarize the livestreamed I/O event, I used the NexusTrade chat and asked the following question.

Do a deep dive on Google’s IO event today

Unlike other AI models which might do a simple web search, the NexusTrade AI is built specifically to answer these types of questions accurately. Because it contains the words “deep dive”, it will do an intense search throughout the web for accurate answers and also give us sources to backtrack on our research.

And poetically, using Google’s newer Gemini 2.5 Flash, I performed this deep research. You can read the full results of the analysis here.

The full report is long, but let me talk about the highlights that really excited me.

Google I/O 2025: An AI Avalanche That Demands Attention

The full report contained details on some of Google’s biggest announcements, including their new image and video generators. I decided to test them out myself and all I’ve got to say…

Wow.

They are not messing around this year.

Imagen 4

Google’s updated Imagen 4 tool is a step beyond even the best image generators from OpenAI and xAi. Unlike these other models, it actually listens to what you want, and generates the image.

Don’t take my word for it. Let’s do a direct comparison.

Let’s take this handsome devil as the input to the model.

And now let’s ask both ChatGPT and Google Gemini to update the image. We’ll use the same exact text prompt.

Regenerate this picture but put me in a suit and tie

The result on the left is the image generated by ChatGPT. The result on the right was generated by Google.

For the ChatGPT image, I don’t know WHO OpenAI generated, but that’s clearly NOT me.

And if you dare say “oh, but it kinda looks like you”, tell me this… If I was in a police lineup and that’s the only image they had of me, am I staying in jail that night?

I could have the victim’s blood literally on my hands. I’m sleeping in my bed THAT NIGHT.

In contrast the image generated by Google IS unmistakably me. It doesn’t really look AI-Generated and I bet with some slice prompt tweaking, I could create a new LinkedIn photo within the hour.

It’s like they dressed me up and plopped me back in the background of the original image. It’s genuinely mind-blowing in comparison.

But what’s crazier than generating high-quality images is generating high-quality videos to go alongside it.

Flow with Veo 3

Flow is Google’s new AI filmmaking tool. It allows the creation of videos from text prompts and photos.

Even with the baseline plan of $20/month, Veo 3 blows Sora out of the water with its quality. To test this, I used the following prompt with both models.

Generate a picture of a passenger plane flying towards the ground with its engines on fire. It then hits the ground and there is a fiery explosion

In this test, this is just greenfield generation — generating directly with a text prompt. And in all honesty, neither video is particularly jaw-dropping.

But Google’s is far better.

It at least follows the image of plane flying, hitting the ground, and a fiery explosion afterwards. Sora is confused about everything, and even detonated the plane before hitting the ground and did a weird camera pan off.

The results aren’t even comparable.

What’s also neat is that the advanced Gemini plan (starting at $125/month) has additional features like 4K video generation and native audio generation. It also has direct picture-to-video generation, which may prove to be invaluable for content creators like me. While inaccessible to the vast majority of AI enthusiasts, including myself, this is a monumental step forward that’s bound to cause aggressive competition in the near future.

Some other interesting things to come out of this event includes:

- Project Mariner: Real-world agentic tasks that can handle things such as buying concert tickets or purchasing groceries

- Project Astra: Augmented-reality that allow for insane use-cases such as live-translation. This is the first direct attack to Meta’s AI Ray-Bans that we’ve seen from any tech company

- Google Workspace enhancements: Some neat improvements to Google workspace including Gemini integration with Google Docs and live translation via Google Meet

While Google’s I/O event was absolutely an unforgettable milestone in the advancement of AI, shiny gadgets and useful tools aren’t enough for me to consider investing.

What’s more important is the overall strength of the business.

Diving Deeper: Is GOOGL a Smart Stock to Buy?

To answer the question of “should I buy Google stock?” , I turned to the Alphabet Inc. (GOOGL) Deep Dive Report generated by NexusTrade.

This report combines:

- Fundamental data from EODHD, a high-quality data provider

- Calculated financial metrics such as compound annual growth rate

- News from a variety of different sources on the internet

And generates a comprehensive, data-backed report that is thorough, robust, and easy to fact-check.

What I found was a compelling, if complex, picture.

Want high-quality fundamental data for your financial platforms? Get started for free on EODHD!

The Financial Fortress:

The report highlights Google’s robust financial performance. We’re talking Q1 2025 revenue of $90.2 billion and a net income of $34.5 billion.

What really caught my eye was the 30.2% quarter-over-quarter surge in net income, signaling improving operational efficiency. Their balance sheet is a fortress: $95.33 billion in cash and short-term investments, with minimal long-term debt ($10.89 billion).

This financial muscle is crucial for funding the ambitious AI projects showcased at Google I/O. The report states, “Alphabet maintains an exceptionally strong balance sheet… providing Alphabet with significant strategic flexibility.”

Growth and Valuation:

Google’s 10-year revenue CAGR of 16.67% is impressive for a company its size. While the 3-year CAGR moderated, the report notes an acceleration in net income growth.

From a valuation standpoint, the report also states that Google appears reasonably valued with a P/E ratio of 19.03 (as of the report date). This is lower than all of the other FANNG stocks.

But it’s not just the P/E ratio that makes it attractive. Apples-to-apples, if we compare Google to… well Apple, the most valuable company on Earth, we see an interesting story.

- Revenue Growth: Google grew at 13.87% vs Apple’s 2.02% — indicating significantly faster top-line growth.

- Gross Margin: Google’s 58.20% is higher than Apple’s 46.21% — showing Google keeps more profit per dollar of revenue.

- Operating Margin: Google edges out with 32.11% vs Apple’s 31.51% — suggesting slightly better operational efficiency.

- Net Margin: Google’s 28.60% vs Apple’s 23.97% — meaning Google converts more revenue into bottom-line profit.

- P/E Ratio: Google trades at 19.03 vs Apple’s 32.48 — making Google cheaper relative to its earnings.

- EV/EBITDA: Google’s multiple is 15.01 vs Apple’s 23.16 — showing Google is priced more attractively based on core operating profit.

This presents an interesting value opportunity. While Apple has things that Google doesn’t have, including brand loyalty, better hardware, and less regulatory scrutiny, Google is the cheaper stock fundamentally.

News Catalysts:

Last but not least, the Deep Dive Report also touched on recent news, like the new “Google AI Ultra” subscription, an extremely expensive recurring subscription for AI fanatics like myself. This paints apicture of a company aggressively pushing into new growth frontiers.

The report also mentioned the fact that Google Waymo is expanding. This is a good segue-way into one of my favorite parts about Google’s businesses that are, for some reason, never talked about.

Insanely wild innovations like self-driving cars.

The Waymo Wildcard: The Self-Driving Future Tesla Dreams Of

One of the most electrifying, yet often underappreciated, parts of Google’s story is its “Other Bets” category. Specifically, it’s long-shots like DeepMind and Waymo.

While Tesla has a dream of creating a fleet of self-driving taxis, Waymo has already made that into a reality. And they are expanding.

The video above perfectly exemplifies this. In Austin, TX, while taking an Uber across the city, the app notified me that I could instead take a Waymo.

I enthusiastically agreed.

While in the Waymo (which was already a fever-dream-like experience, looking to my left, and seeing no driver with the wheel turning itself). I noticed two other Waymos around me on the street.

It was a real-world Sci-Fi movie.

It felt like stepping directly into the future. The fact that you can blabber loudly or blast your music or act like a belligerent idiot (for fun!) with no consequences is absolutely unbelievable… and surreal.

The fact that Google is a leader in this multi-billion dollar industry is a massive, often overlooked, upside. Why isn’t this the headline when people discuss what stocks to buy for long-term disruptive growth? Why does Tesla make headlines for this and they don’t even have a real fleet?

The “Yeah, Buts”: Acknowledging Google’s Risks

Now, it’s not all sunshine and rainbows. The Deep Dive Report rightly assigns Google a “Medium” overall risk rating. The biggest elephant in the room is regulatory scrutiny. Antitrust lawsuits and investigations are ongoing globally, and these could lead to significant fines or forced changes to their business model.

There’s also the dependency on search advertising. While diversifying, search remains the cash cow. The report highlights the threat of “AI-powered alternatives potentially diminishing traditional search usage.”

This is a real concern. Google’s search volume HAS decreased for the first time in two decades. The big question is, can Google navigate the shift to AI-driven information retrieval without cannibalizing its golden goose?

With the massive amounts of cash stockpiles and the historical increase in operational efficiency, my guess would be YES. But it’s no guarantee.

We see from the Google I/O event that they are trying, but the execution risk is there. Competition in AI is also fierce, with giants like Microsoft, Meta, and OpenAI all vying for dominance.

Why I’m Taking a Small Bite of the Apple (or, Google)

Despite these risks, the Google I/O 2025 announcements, combined with my experience riding in a Waymo and the insights I learned from the Deep Dive Report have convinced me to start building a small position in GOOGL. My NVIDIA success has given me the flexibility to make calculated bets, and Google’s AI trajectory is incredibly compelling.

The company’s financial strength provides a safety net, and its investments in AI are aggressively offensive. The potential for AI to enhance every single one of their products — from Search and YouTube to Cloud and Android — is immense.

And then there’s Google’s “Other Bets” segment. This of course includes Waymo, my personal favorite taxi experiment. But it also includes other niche applications, like DeepMind and AlphaFold, an AI algorithm that all but solved the 70-year-old infamous “Protein Folding Problem”.

These AI innovations WILL change the world, even if it weakens its money-printing search segments.

I’ve seen firsthand how AI can generate market-beating trading strategies. Now, I’m betting on a company that is at the forefront of building that AI. It’s a long-term play, and I’m aware of the hurdles. But the potential upside, especially given its current valuation relative to some peers, makes it an attractive consideration for “what stocks to buy” for an AI-centric future.

Final Thoughts: Is Google the Next Big Play?

Google I/O 2025 was a powerful statement about the future of technology. For investors wondering “what stocks to buy” to capitalize on the AI revolution, Google (GOOGL) presents a fascinating case. It has the brains, the brawn, and now, a crystal-clear roadmap for an AI-driven future.

For these reasons, I’m cautiously starting a long-term Google trading setup.

My AI-Powered Due Diligence (powered by NexusTrade) has allowed me to see incredible success with NVIDIA. While I’m mostly in cash, the sheer innovative power displayed by Google, backed by solid fundamentals, was too compelling for me to ignore.

It’s a calculated risk, but one I’m willing to take.

What do you think? Is Google on your “stocks to buy” list after I/O? Leave a comment and share what you thought of the conference!

Follow me: LinkedIn | X (Twitter) | TikTok | Instagram | Newsletter

Want to conduct your own deep dive analysis or create AI-powered trading strategies? Check out NexusTrade.io — the platform I built to bring institutional-grade tools to retail investors.

No comments yet.